Choosing a way to finance your next car isn’t just a hunt for the lowest interest rate anymore. According to the latest Lending Indicators from the ABS, Australians are still signing up for roughly $4.9 billion in vehicle loans every single quarter.

However, the current financial landscape has shifted, making tax-smart structures more competitive than ever. Whether you are looking at a traditional petrol engine or a new EV, this guide dives into the novated lease vs car loan debate to show you exactly which path puts the most cash back into your pocket.

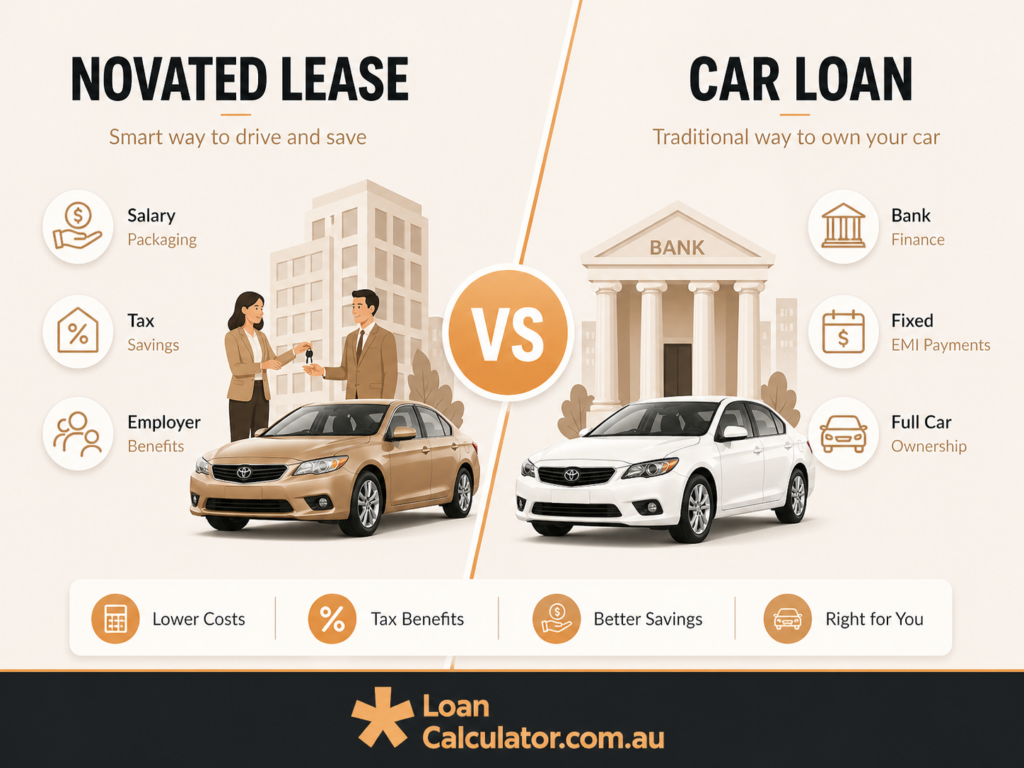

Comparing the Basics: What Are Novated Leases and Car Loans?

Each financing option, car loans and novated leases, operates on a distinct financial framework. Let’s examine how these two structures affect your disposable income.

Understanding the Novated Lease Structure:

A novated lease is a three-way agreement between you, your employer, and a finance provider. Your lease payments and all car running costs (fuel/charging, insurance, rego) are deducted from your salary by your employer, partially from your pre-tax income, reducing your overall taxable income.

The Traditional Car Loan Explained:

A car loan is a straightforward personal finance agreement where a lender provides the funds to purchase a vehicle up front. You own the car from day one, and you make regular repayments using your after-tax salary, with no involvement from your employer.

Novated Lease vs Car Loan: Total Cost Comparison (2026 Breakdown)

When comparing a novated lease to a car loan, the real difference is not just the monthly payment, but how much of your ‘gross’ salary stays in your pocket versus going to the ATO. This section breaks down the mechanical differences in cost, specifically highlighting how the current tax year’s thresholds create significant savings for eligible drivers.

The All-inclusive Finance Comparison between Novated Lease and Car Loan:

| Feature | Novated Lease | Traditional Secured Car Loan |

| Payment Source | Pre-tax & Post-tax salary. Uses gross income to reduce tax. | 100% After-tax salary. Paid from your take-home pay. |

| Upfront GST Saving | Exempt. Save 1/11th of the price (up to $6,334). | Paid in full. No GST credit available for individuals. |

| Income Tax Benefit | Yes. Lowers your taxable income bracket. | No. No impact on your taxable income. |

| Running Cost GST | 10% Saving. No GST on fuel, tyres, or servicing. | None. You pay full retail price for all costs. |

| EV FBT Status | 0% Tax. Exempt if under $91,387 (LCT limit). | N/A. No tax benefits for choosing an EV. |

| Luxury Car Tax | Applied over $91,387 (EV) / $80,567 (Other). | Applied over $91,387 (EV) / $80,567 (Other). |

| Ownership | Residual/Balloon payment required at the end. | You own the asset from Day 1. |

| Job Portability | Must be ‘re-novated’ if you switch employers. | Independent of your employment status. |

| Budgeting Style | All-inclusive. One payment covers finance & costs. | Variable. Separate bills for rego, fuel, and repairs. |

Pros and Cons of Novated Lease vs Car Loan Based on Your Financial Priorities

Your ‘winner’ depends on whether you value immediate tax savings or long-term flexibility and total ownership.

Advantages and Disadvantages of a Novated Lease

This section explores how a three-way salary packaging agreement can lower your taxable income while acknowledging the obligations that come with employer-tied finance.

| Novated Lease Pros: | Novated Lease Cons: |

|---|---|

| ✅ Tax Wins: Lowers your taxable income, which could potentially nudge you into a lower tax bracket. | ❌ Residual Payment: You must pay a ‘balloon’ amount at the end if you want to keep the car. |

| ✅ GST Savings: You skip the 10% GST on the car’s purchase price and on all ongoing running costs. | ❌ Employment Link: If you leave your job, the lease ‘de-novates’ and becomes a private, often more expensive, monthly bill. |

| ✅ All-in-One: Fuel, insurance, and servicing are bundled into one simple, automated deduction. | |

| ✅ EV Incentives: 2026 is a massive year for FBT-exempt electric vehicles, offering peak savings. |

The Benefits and Drawbacks of a Traditional Car Loan

Below, we analyse why traditional lending remains the go-to for car owners prioritising full autonomy and straightforward ownership without workplace involvement.

| Car Loan Pros: | Car Loan Cons: |

|---|---|

| ✅ Full Control: You choose your insurer, your mechanic, and when you want to sell the vehicle. | ❌ Zero Tax Relief: Every dollar spent on the car and interest is earned after the government takes its cut. |

| ✅ No Employer Link: Your car finance is not tied to your employment status. | ❌ Depreciation: You bear the full brunt of the car’s value drop without any tax offsets. |

| ✅ Simple Structure: No complex salary sacrifice or FBT reporting required. |

Common Mistakes to Avoid When Financing a Car

In the current financial landscape, sticking to 2020-era logic can lead to expensive oversights. Here are the most critical mistakes to avoid when weighing your options.

- Ignoring the PHEV Eligibility Cut-off:

As of 1 April 2025, plug-in hybrid electric vehicles (PHEVs) are no longer eligible for the electric car FBT exemption. Financing a PHEV under the assumption it is ‘tax-free’ can skew your cost comparison significantly. - Overlooking the RFBA Impact:

Even if your EV is FBT-exempt, it appears as a Reportable Fringe Benefit Amount (RFBA) on your income statement. This figure is used to calculate compulsory repayments for HECS/HELP debt, potentially increasing your annual obligations. - Focusing Solely on Interest Rates:

Don’t compare options by interest rates alone. While a car loan may have a lower rate, it lacks the tax benefits of salary sacrificing. Because lease payments use pre-tax dollars to reduce your taxable income, the total savings can often outweigh a higher interest rate. - Miscalculating the Luxury Car Tax (LCT):

For the 2025-26 period, the LCT threshold is $91,387 for fuel-efficient vehicles and $80,567 for others. Crossing these thresholds adds a 33% tax to the amount above the limit, which must be factored into your monthly budget. - The Residual Payment Trap:

Many drivers forget to account for the minimum residual payment required by the ATO at the end of a lease. Without a savings plan for this balloon payment, you may be forced to refinance the remaining balance at current market rates.

Tax Benefits and Cost Savings:

A novated lease acts as a strategic tax-optimisation tool, whereas a car loan is a standard debt agreement. This choice determines whether you pay the ATO more than necessary or retain that income through salary packaging.

The ‘Tax Shield’: Paying with Pre-Tax vs. Post-Tax Income

A novated lease allows you to pay for your vehicle using gross salary before income tax is applied, effectively lowering your taxable income. In contrast, a car loan provides no tax relief, requiring all repayments to come from your ‘net’ take-home pay after the government has already taken its cut.

Cost Incentives: GST Credits and the EV Advantage

Leasing provides an immediate edge by removing the GST on the purchase price, up to the ATO’s limit, and on all ongoing running costs. Furthermore, qualifying Battery Electric Vehicles (BEVs) remain FBT-exempt in 2026, offering a ‘double-dip’ saving that makes leasing significantly cheaper than a traditional loan for green car buyers.

The right choice depends on your specific financial profile. When comparing a novated lease vs. a car loan, high-income earners or those switching to a Battery Electric Vehicle (BEV) will find that GST and FBT exemptions make the lease mathematically superior.

However, if you prefer full ownership or fall into a lower tax bracket with fewer packaging benefits, a secured car loan offers the most flexibility. Always use a repayment calculator to compare the ‘Net Effect’ on your take-home pay before signing any contracts.