Menu

Getting a loan involves more than just the price tag of the bike. Breaking down the main parts of a contract makes it easy to budget for the whole life of your loan.

This is the fee a lender charges to borrow their money, setting your payment size. Rates vary based on the lender, market conditions, and whether you pick a fixed or variable setup.

Australian lenders offer terms from one to seven years. Shorter terms mean higher regular payments but less interest overall. Longer terms lower your ongoing bills but cost more in the long run.

Putting cash down upfront means you borrow less overall. This immediately shrinks your regular bills. It also proves to lenders you are a safer applicant, which can help you score a much lower interest rate.

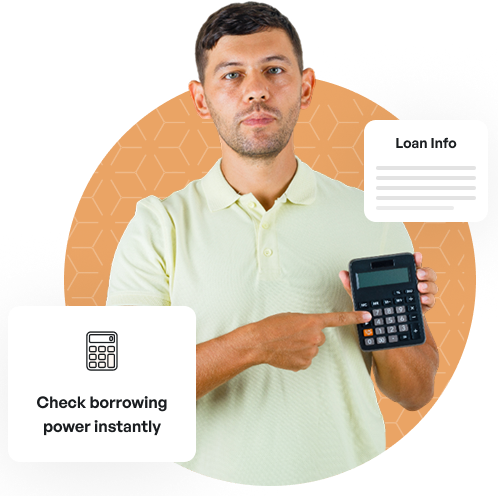

Going in with real data gives you confidence. You will know exactly how a small shift in interest rates affects your wallet, helping you spot a good deal and avoid sales pitches.

With a secured loan, the lender uses the motorbike itself as a guarantee until you pay the debt off in full. Because this setup reduces the risk for the lender, they will usually give you a much lower interest rate.

An unsecured loan does not use the motorcycle as a guarantee, so the lender relies entirely on your credit history instead. While your bike isn’t at risk if you fall behind, these loans usually come with higher interest rates to cover the lender’s extra risk.

Financing a brand-new model fresh off the showroom floor often qualifies you for highly competitive interest rates from lenders. This is because new bikes retain predictable market values and represent a highly reliable form of security for the financial institution.

Going secondhand saves you money upfront and lets you dodge the major drop in value that hits new bikes the second they leave the shop. Just look out for the vehicle’s age; lenders often charge a bit more interest or give you fewer years to pay it off if the bike is older.

The final bill depends on your personal finances, the bike you choose, and how you set up the loan. Tweaking these numbers can help you land a much better deal.

This is how long you take to pay back the debt. Spreading the balance over more years lowers your regular payments but means you pay interest for longer.

Checking the basic rules and gathering your paperwork early speeds up the approval process. Lenders look for a few specific criteria and documents to move your application forward.

Use our calculator to test different amounts and find a payment size you are comfortable with.

Look at your credit history early so you can fix any issues and get the right interest rates.

Gather your payslips, bank statements, and ID to stop any delays later on.

Get a clear spending limit from a lender before you choose your bike.

Share the bike details with your lender so they can pay the seller and finish the deal.

For security purposes, please solve this simple puzzle to verify you are human before sending an OTP.