Buying a new set of wheels is exciting, but tracking down the right finance can feel overwhelming. While finding the vehicle is half the battle, understanding how you pay for it determines the car’s true cost over the long run.

Fortunately, getting a handle on the basics is simple. In this read, we break down exactly how car loans work so you can confidently pick a finance setup that fits your lifestyle.

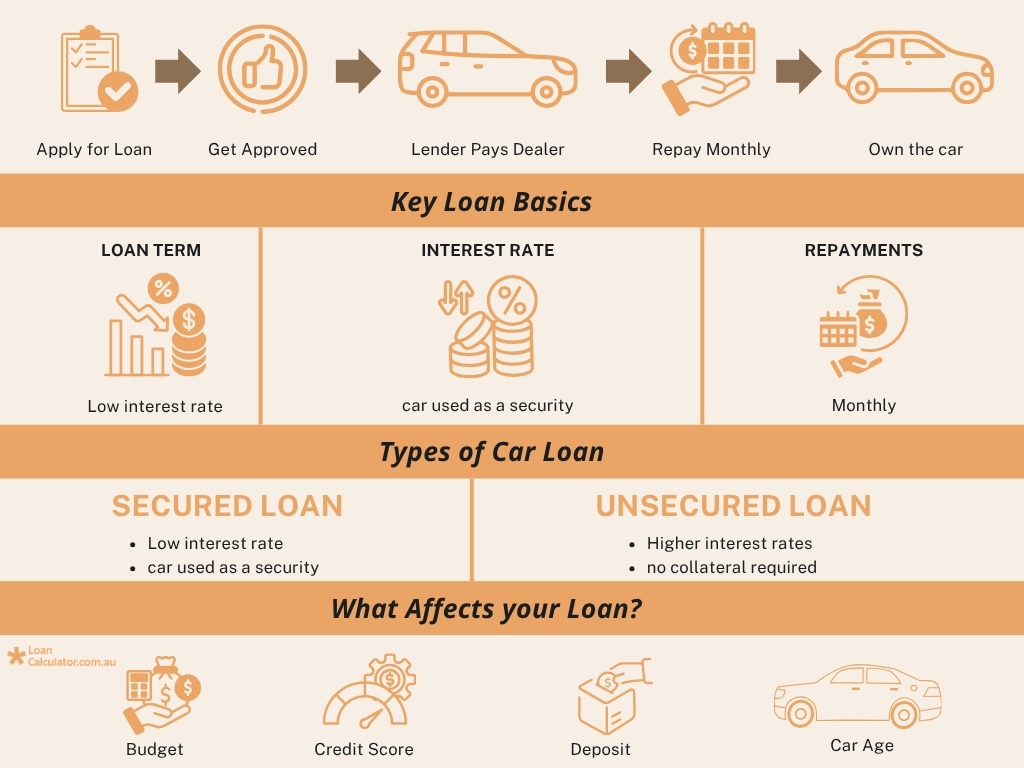

Understanding How Car Loans Work

A car loan is a straightforward agreement where a lender covers the upfront cost of your vehicle, and you pay them back over time. Each regular payment reduces what you owe while covering the cost of borrowing the money.

- You borrow a specific amount of money to pay for your car.

- You pay that money back over an agreed timeframe, usually between one and seven years.

- The lender adds interest to your balance for borrowing the money.

- You make your regular payments on a schedule that fits your cash flow, like weekly, fortnightly, or monthly.

Want to estimate your car loan repayments in Australia?

Use our Car Loan Calculator to see how much your loan could cost based on interest rates, loan terms, and your budget. It’s quick, simple, and helps you plan with confidence before applying.

Different Types of Car Loans Explained

Car finance options look different depending on how you structure your contract and what you plan to use the vehicle for. Every option comes with its own set of rules around ownership, interest, and how you pay the money back.

- Secured Loans: You use the car as a backup for the loan. If you cannot make your payments, the lender can take the vehicle. Because this lowers the risk for them, you often get a much better interest rate.

- Unsecured Loans: You do not have to offer the car as backup. Since the lender takes on more risk, they will look much closer at your income and generally charge higher interest rates. This is common if the car you want is too old to be used as security.

- New Car Financing: This is specifically for brand-new vehicles bought from a dealer or maker. Lenders love new cars because they hold their value better, which can make getting a competitive rate much easier.

- Used Car Financing: This covers any vehicle that has had a previous owner. Lenders will usually check the car’s age and condition before they agree to the loan terms, and some would not finance cars over a certain age.

- Fixed-rate Options: Your interest rate stays locked in from day one until your very last payment. Your regular costs never change, which makes planning your personal budget incredibly easy.

- Variable-rate Options: Your interest rate can move up or down depending on what happens in the wider financial market. This means your regular payments can change over time, making your costs a bit harder to predict.

- Dealer Finance: The dealership sets up this loan for you right on the showroom floor while you are buying the car. While it is highly convenient, it pays to check the rates against outside options before signing on the dotted line.

- Balloon Payment Contracts: You make lower regular payments during the loan term, but you leave a large lump sum to pay off at the very end. It keeps your ongoing costs down, but you must be ready for that final bill if you want to own the car outright.

Main Factors That Affect Car Loan Repayments and Interest Rates

Lenders look at a few main details before offering a car loan. These factors decide your regular bill size and how much extra you pay in the long run.

- How Much You Borrow: A bigger loan means higher regular payments and more total interest built up over time.

- The Length of the Loan: Spreading your loan over more years lowers your individual bills, but it increases the total interest you pay overall.

- The Interest Rate: A higher percentage pushes your regular payments up and makes the car more expensive.

- Your Credit History: A clean track record with money gives lenders confidence, helping you get lower interest rates.

How to Calculate Car Loan Repayments Using an Online Calculator

An online tool takes the guesswork out of your budget by showing you what your future bills might look like. It lets you test different numbers safely from home before you ever speak to a lender or fill out an application.

- Plug in the Basics: You type in the price of the car, the interest rate you expect, and how many years you want to take to pay it off.

- See the True Cost: The calculator instantly estimates your regular payments so you can see if they fit comfortably into your wallet.

- Play With the Numbers: You can easily change the values, like shortening the timeframe or adding a deposit, to see exactly how it shifts your ongoing costs.

- See the Bigger Picture: Once you find the right numbers, you can use our platform to compare matching options from 40+ lenders across Australia.

Comparing Car Loan Options from Multiple Lenders

Comparing multiple lenders helps you understand how loan offers can differ in terms of rates, features, and repayment structures. It allows you to view different options side-by-side before making a decision.

| Lender Type | Interest Rate Type | Loan Term Range | Repayment Frequency | Key Feature |

|---|---|---|---|---|

| Bank Lenders | Fixed/Variable | 1-7 years | Weekly/Fortnightly/Monthly | Structured approval process |

| Credit Unions | Fixed | 1-7 years | Weekly/Monthly | Member-focused lending |

| Online Lenders | Fixed/Variable | 1-7 years | Flexible options | Faster application process |

| Dealer Finance | Fixed | 1-7 years | Monthly | Offered at the point of sale |

Ready to see what your car loan could look like?

Use our calculator to estimate your repayments and find a loan that fits your budget today.

Key Takeaways

Getting a car loan comes down to managing three main puzzle pieces: how much you borrow, your interest rate, and how long you take to pay it back. When you understand how these elements connect, it is much easier to see exactly how car loans work and find a setup that fits your lifestyle.

Using independent calculators and comparison tools lets you test different numbers safely from home before you apply. This quickly shows you how stretching out a loan lowers your regular bills but increases your total interest, helping you choose the right plan.